Monkey Business Images // Shutterstock

Understanding the Timeline for Car Insurance Claims

After a car accident, one of the most pressing concerns for drivers is how long it will take to settle their insurance claim. The timeline can vary significantly depending on the nature of the incident, state laws, and the efficiency of the insurance company. While simple claims might be resolved in just a few days, more complicated cases could stretch over weeks or even months. To help you navigate this process, we’ll explore the factors that influence claim settlement times and what you can expect throughout the process.

When to File a Car Insurance Claim

Filing a claim isn’t always the best option, especially for minor incidents. Before deciding to file, consider whether the cost of repairs exceeds your deductible. A deductible is the amount you pay out of pocket before your insurance coverage begins.

For example, if your deductible is $1,000 and the repair cost is only $500, it may not be worth filing a claim. In this case, you would end up paying the full cost yourself and still risk a potential rate increase. However, there are situations where filing a claim is necessary:

- Injuries are involved: Medical costs can add up quickly, and your liability coverage is meant to protect you from significant financial loss in such cases.

- The accident involves another party: This includes other vehicles, property (like a fence or building), or pedestrians. Your insurance company will need to handle liability and any potential legal issues.

- The at-fault party is unclear: If there’s a dispute over who caused the accident, your insurance company can assist in investigating and determining fault.

- Damage is significant: If the repair costs are much higher than your deductible, filing a claim makes financial sense.

How Long Do Insurance Companies Have to Settle a Claim?

Insurance companies are required to follow state-specific laws regarding claim settlement timelines. These laws are designed to prevent unreasonable delays and protect consumers. While most states require insurers to act “promptly,” some have specific deadlines that must be followed.

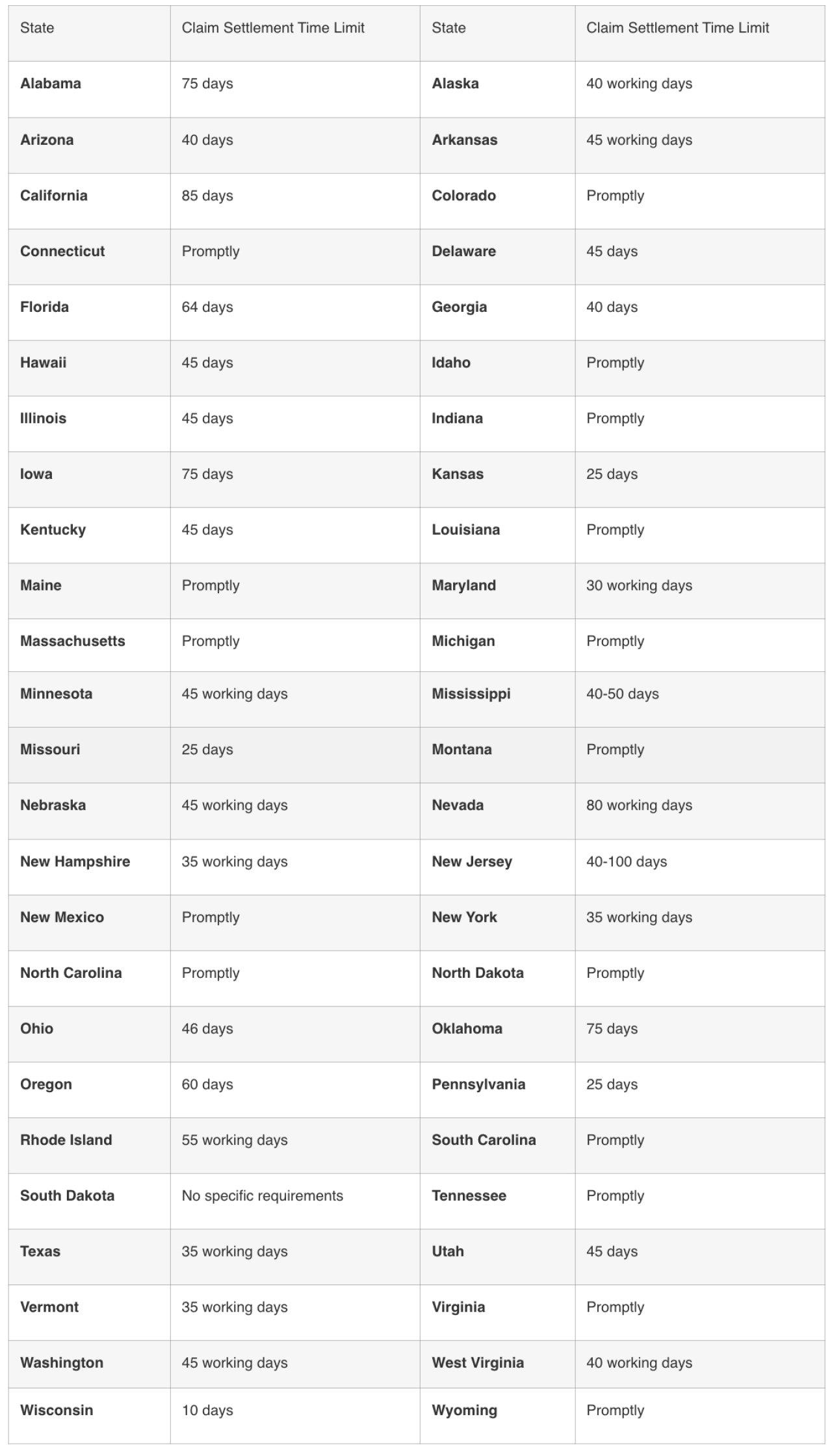

Here is a general overview of state-specific claim settlement time limits:

CheapInsurance.com

Factors That Influence Claim Settlement Time

The length of time a claim takes to settle is directly related to its complexity.

Simple Claims

These are typically resolved quickly. They involve minor damage, clear liability (who is at fault), and no injuries. Examples include a broken windshield, minor scratches, or a roadside assistance call.

Complex Claims

These take longer to settle because they require more investigation. These claims often involve:

- Bodily Injury: Medical claims can be time-consuming to process as the full extent of the injuries may not be known immediately. The claims adjuster needs to review medical records, bills, and potentially speak with doctors.

- Disputed Liability: If both parties claim the other is at fault, the insurer will need to collect evidence, interview witnesses, and review police reports to determine who is liable.

- Total Loss: If a vehicle is considered a total loss, the insurer must determine its actual cash value (ACV), which involves researching its market value, condition, and mileage. This process can take several weeks.

For complex claims, it can be helpful to be familiar with the common insurance terms.

What to Do If Your Claim Is Delayed

If you feel your insurance company is taking too long, don’t just wait. You can take action to keep the process moving.

- Communicate Proactively: Regularly check in with your insurance adjuster to get a status update. Ask for a specific timeline for the next steps and make sure you have provided all the information they need.

- Document Everything: Keep a detailed log of all communication, including dates, times, and the names of the people you spoke with.

- File a Complaint: If the delay is unreasonable and the insurer is not providing a clear reason, you can contact your state’s Department of Insurance. They can mediate the situation and enforce the state’s claim settlement laws. In extreme cases, if the insurer acts in bad faith, you may have grounds to pursue legal action.

By understanding the claims process and being proactive, you can help ensure your claim is settled as efficiently as possible.