The Impact of Expiring Health Insurance Subsidies

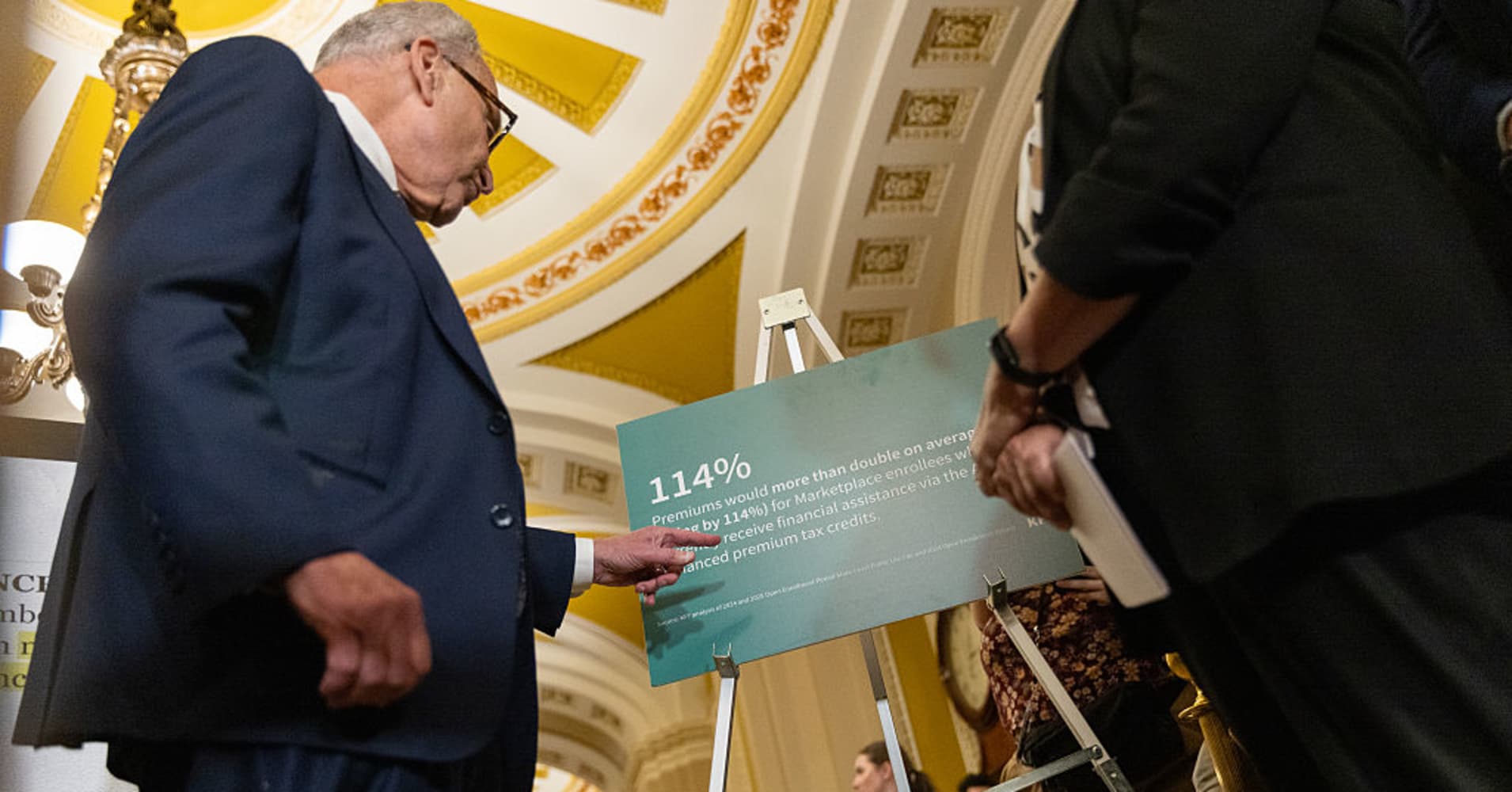

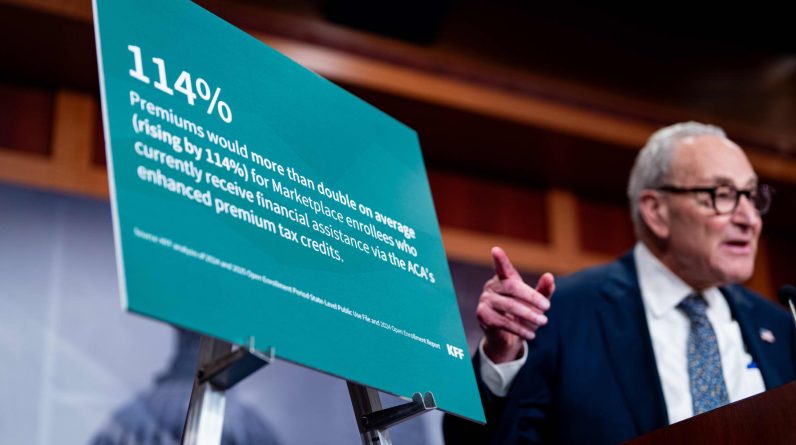

Health insurance premiums for plans purchased through the Affordable Care Act (ACA) marketplace could see a dramatic increase if enhanced subsidies expire at the end of the year. According to an analysis by KFF, a nonpartisan health policy research group, the average premium would rise by 114%. This significant jump would affect millions of Americans who currently rely on these subsidies to make their health insurance more affordable.

The issue has become a focal point in ongoing political negotiations as Democrats push to extend the enhanced “premium tax credits” as part of a deal to prevent a government shutdown. These subsidies help reduce the cost of health insurance for approximately 22 million ACA enrollees. Without them, the financial burden on these individuals could become overwhelming.

What Are Enhanced Premium Tax Credits?

Premium tax credits were initially established under the Affordable Care Act and were available for households with incomes between 100% and 400% of the federal poverty level. In 2021, the American Rescue Plan Act temporarily increased the amount of these credits and expanded eligibility to include households earning more than 400% of the federal poverty level. For example, this includes a family of four with an income exceeding $128,600 in 2025.

The law also set a cap on the amount a household pays out of pocket toward insurance premiums at 8.5% of their income. These changes were designed to make health insurance more accessible and affordable for a broader range of Americans.

Recent Legislative Actions

Democrats extended the enhanced subsidies temporarily through the Inflation Reduction Act, which was signed into law by former President Joe Biden in 2022. According to KFF, these subsidies saved recipients an average of $705 annually in 2024 on their health premiums.

However, the current debate centers around whether these subsidies should be extended beyond 2025. Republicans argue that negotiations on continuing these credits should occur after the Senate approves a funding resolution. Meanwhile, Democrats are seeking to include the extension of these subsidies as part of a broader deal to fully fund the federal government in fiscal year 2026.

Potential Consequences of Expiration

If the enhanced subsidies expire, the impact on consumers could be severe. KFF’s analysis suggests that the average premium for ACA plans would jump from $888 this year to $1,906 in 2026 — a 114% increase. This would place a significant strain on families and individuals already struggling with the rising cost of healthcare.

Other factors could further compound the cost increase for enrollees. For instance, the Trump administration changed the way tax credits are calculated, resulting in enrollees paying a higher share of their income toward a benchmark ACA plan in 2026. Additionally, insurers have proposed raising rates by a median of 18%, due to rising healthcare costs and the expiration of enhanced subsidies. This would mark the largest rate increase since 2018.

Real-World Examples

KFF’s findings highlight the varied impact of the potential premium increases across different income groups. For example, a 60-year-old couple making $85,000 — or 402% of the federal poverty level — would see their yearly premium payments rise by over $22,600 next year after accounting for the loss of enhanced credits and insurers’ rate increases.

In another scenario, a 45-year-old earning $20,000 — or 128% of the federal poverty level — in a state that hasn’t expanded Medicaid coverage would see premiums for a benchmark health plan rise from $0 to $420 per year, on average, due to the loss of enhanced premium tax credits.

Broader Implications

The expiration of enhanced subsidies could have far-reaching implications for the ACA marketplace and the millions of Americans who depend on it. As the debate continues, the outcome will significantly affect the affordability and accessibility of health insurance for many families across the country.